https://www.cato.org/policy-analysis/comprehensive-evaluation-policy-rate-feedback-rules

https://www.cato.org/policy-analysis/comprehensive-evaluation-policy-rate-feedback-rules

권호기사보기

| 기사명 | 저자명 | 페이지 | 원문 | 기사목차 |

|---|

| 대표형(전거형, Authority) | 생물정보 | 이형(異形, Variant) | 소속 | 직위 | 직업 | 활동분야 | 주기 | 서지 | |

|---|---|---|---|---|---|---|---|---|---|

| 연구/단체명을 입력해주세요. | |||||||||

|

|

|

|

|

|

* 주제를 선택하시면 검색 상세로 이동합니다.

Title page

Contents

EXECUTIVE SUMMARY 1

INTRODUCTION 2

BENEFITS OF RULES-BASED MONETARY POLICY 2

COMPARISON OF FEEDBACK RULE INFORMATION BURDENS 3

STRUCTURAL MACROECONOMIC ANALYSIS 6

CONCLUSION 13

ACKNOWLEDGMENTS 14

APPENDIX 14

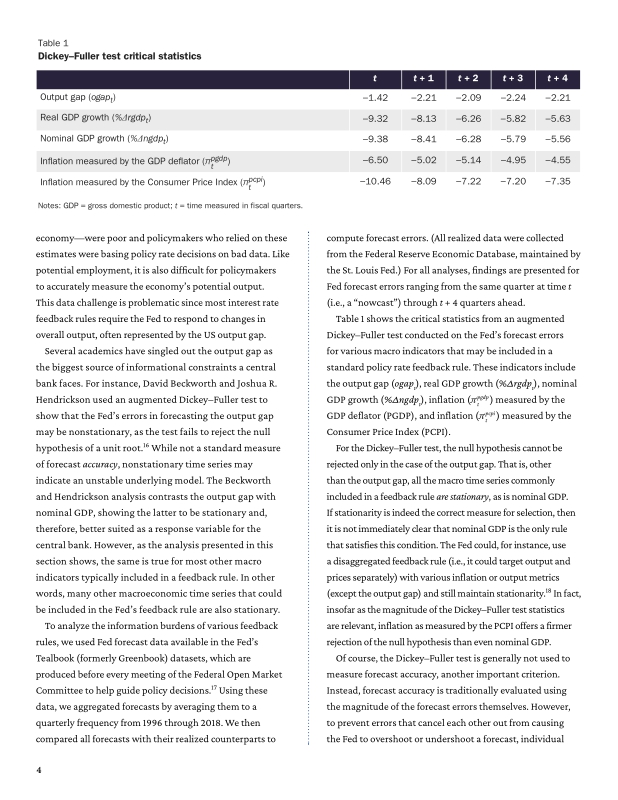

Table 1. Dickey-Fuller test critical statistics 4

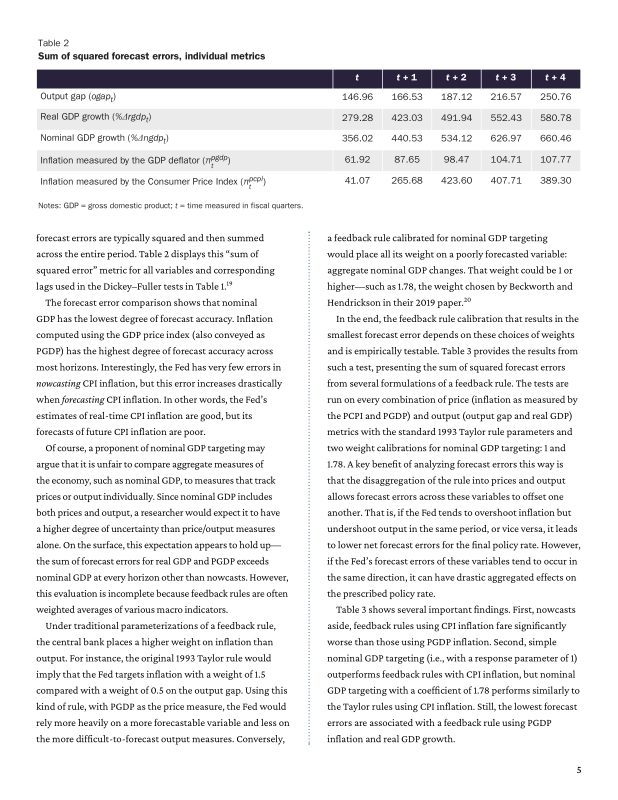

Table 2. Sum of squared forecast errors, individual metrics 5

Table 3. Sum of squared forecast errors, weighted for inclusion in a feedback rule 6

Table 4. Squared and summed impulse responses by shock source and policy rule 10

Table 5. Standard deviation of key macro variables by policy rule 12

Table A1. Squared and summed impulse responses by shock source and policy rule 14

Good monetary policy is important because money is the means of payment for all products and services. A central bank’s failures are particularly damaging because they can create inflation and unsustainable economic gains, producing macroeconomic instability. Given the existing framework of centrally managed fiat money in the United States, Congress can greatly improve monetary policy by, among other things, requiring the central bank to follow a policy rule. Requiring the Federal Reserve (Fed) to follow a policy rule would anchor the public’s expectations for monetary policy actions, improve economic outcomes, and increase accountability for both elected and appointed government officials. Properly structured, a policy rule would also provide Fed officials with the ability to change their stance, provided they give Congress a complete explanation of why they deviated from the rule. This paper uses empirical evidence to demonstrate that most commonly accepted monetary policy rules share a similar framework and that each has its own benefits and costs—that is, no one rule is better than all others. Therefore, any disagreements over which rule is best should not prevent Congress from requiring the Fed to adopt and follow one.

*표시는 필수 입력사항입니다.

| *전화번호 | ※ '-' 없이 휴대폰번호를 입력하세요 |

|---|

| 기사명 | 저자명 | 페이지 | 원문 | 기사목차 |

|---|

| 번호 | 발행일자 | 권호명 | 제본정보 | 자료실 | 원문 | 신청 페이지 |

|---|

도서위치안내: / 서가번호:

우편복사 목록담기를 완료하였습니다.

*표시는 필수 입력사항입니다.

저장 되었습니다.